Morgan Stanley’s proposed 0.14% ETH and SOL fees could turn the next crypto ETF race into a price fight

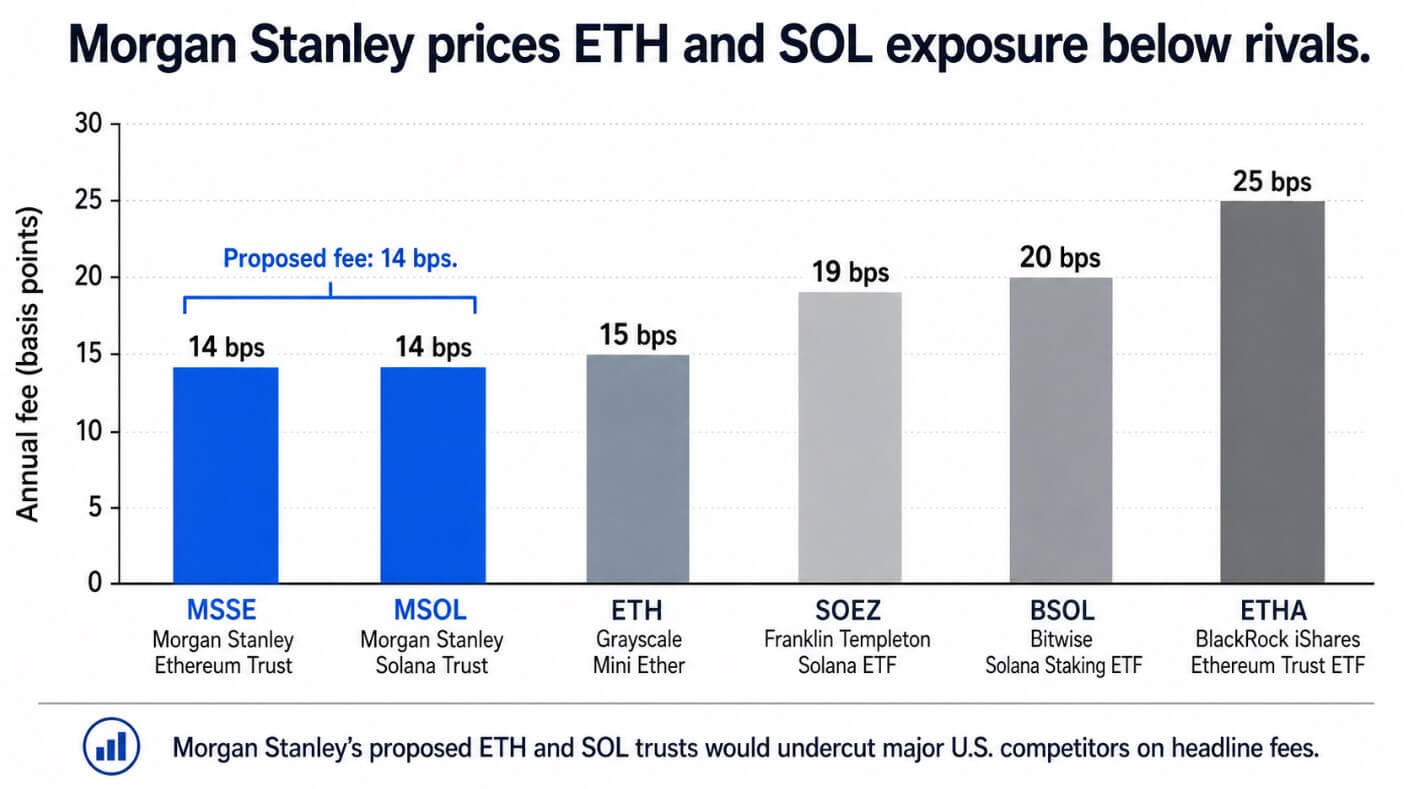

Morgan Stanley filed amended registration statements for proposed Ethereum and Solana ETF trusts on June 18, setting a 0.14% annual delegated sponsor fee on both products.

Bloomberg senior ETF analyst Eric Balchunas described the proposed fee as the lowest among ETH and SOL products worldwide.

The ETH trust, expected to trade on NYSE Arca under the ticker MSSE, intends to track ether and staking rewards from a portion of its holdings. The SOL trust (MSOL) intends to stake up to 100% of its Solana.

BlackRock’s iShares Ethereum Trust ETF (ETHA) carries a 0.25% sponsor fee, Grayscale’s mini Ether (ETH) product sits at 0.15%, Bitwise’s Solana staking ETF (BSOL) launched at 0.20%, and Franklin Templeton’s Solana ETF (SOEZ) lists a 0.19% net expense ratio.

The filings are preliminary, and the SEC must declare both registration statements effective before shares trade; neither filing has reached that threshold.

The fee as a position

Morgan Stanley’s 14 basis points on a crypto ETF is a statement about where the firm expects the institutional allocation conversation to go.

Bitcoin ETFs resolved the access problem for institutions, with BlackRock’s IBIT crossing $70 billion in assets under management within 18 months of launch.

The next question for wealth managers and advisors is whether ETH and SOL, packaged cheaply and reliably enough, can occupy a second line in a digital asset sleeve alongside Bitcoin.

Morgan Stanley’s 0.14% fee positions those products as portfolio-building blocks before the allocation question has a broadly accepted answer.

The ETH trust intends to stake 50% to 80% of its holdings under normal market conditions, with staking service providers and custodians receiving an expected aggregate 5% of rewards and the trust retaining the remainder.

The SOL trust extends that model further, allowing up to 100% of holdings to be staked under the same 95% trust-retention structure, with the delegated sponsor explicitly receiving no portion of staking rewards.

Using Bitwise’s disclosed contemporaneous gross staking reward rate of 6.28% as a market benchmark, a fully staked SOL product that retains 95% of rewards would generate roughly 5.97% before the 14 bps fee.

For ETH, at a hypothetical 3% gross staking yield with 50% to 80% staked, the retained staking contribution lands between roughly 1.29% and 2.14% after fees.

Advisors comparing these products are comparing fee-minus-staking economics, such as the gross yield, the staked share, and the trust’s 95% retention rate, which together determine the effective cost of exposure.

| Product | Headline fee | Staking share | Trust reward retention | Illustrative retained yield before fee | Illustrative net after fee |

|---|---|---|---|---|---|

| Morgan Stanley ETH Trust | 0.14% | 50%–80% of ETH | 95% | 1.43%–2.28% | 1.29%–2.14% |

| Morgan Stanley SOL Trust | 0.14% | Up to 100% of SOL | 95% | 5.97% | 5.83% |

What the flow data supports

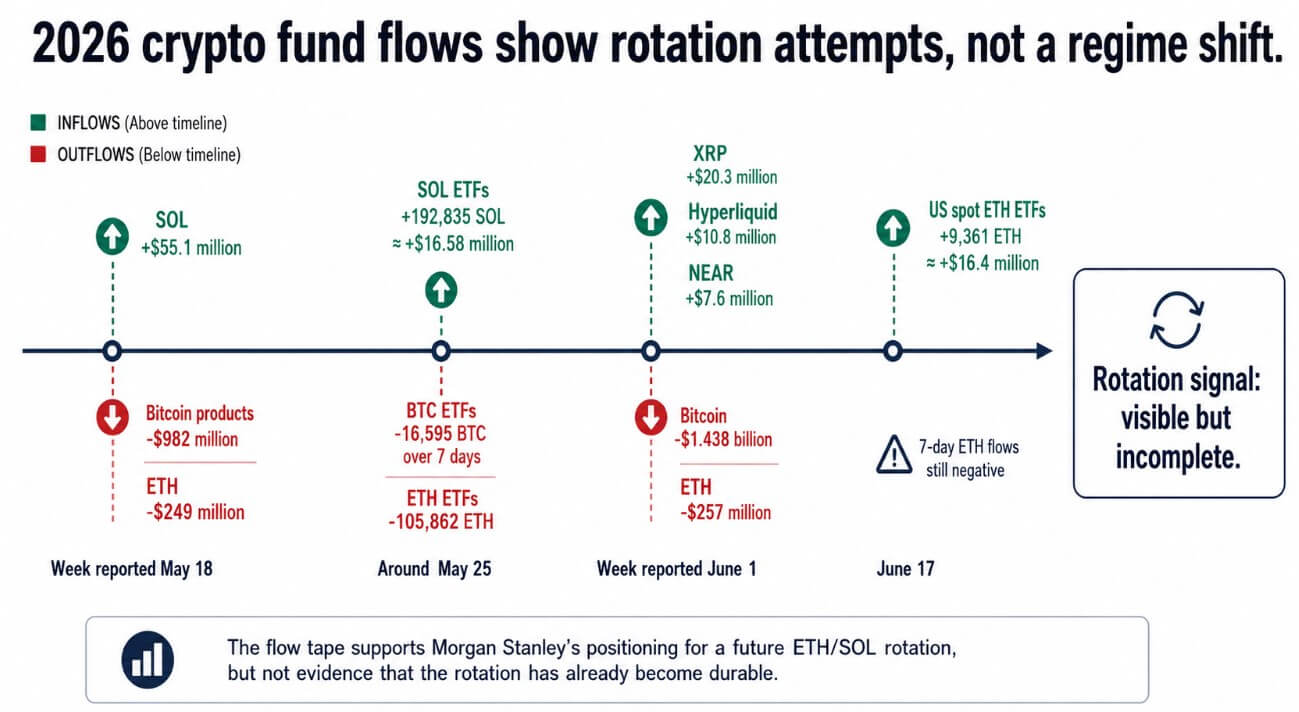

Institutional rotation into ETH and SOL has occurred in fits and starts throughout 2026, with episodic demand and no durable regime in place.

CoinShares’ week reported May 18 showed Bitcoin products absorbing $982 million in outflows, while SOL drew $55.1 million in inflows and ETH saw $249 million leave.

Around May 25, US spot ETF data showed BTC ETFs losing roughly 16,595 BTC over seven days while SOL ETFs added 192,835 SOL, approximately $16.58 million, as ETH ETFs shed 105,862 ETH.

By the week reported June 1, BTC saw $1.44 billion in outflows and ETH $257 million, while the positive pockets were XRP at $20.3 million, Hyperliquid at $10.8 million, and NEAR at $7.6 million.

On June 17, US spot ETH ETFs posted a single-day inflow of 9,361 ETH, approximately $16.4 million, with seven-day ETH flows still negative at week’s end.

The pattern across those weeks is SOL picking up episodic demand while ETH lags behind Bitcoin’s own outflow pace, with alt-specific bids landing on XRP and Hyperliquid, and the ETH/SOL pair failing to attract a sustained bid as a unit.

Morgan Stanley is positioning for a rotation that the data show as episodic and incomplete. The bank operates across 42 countries, and Morgan Stanley Investment Management reported approximately $1.8 trillion in assets under management or supervision as of Sept. 30, 2025.

That distribution reach means a 14 bps fee is also a bid for advisor shelf space. When a wealth manager at a Morgan Stanley branch decides to add non-Bitcoin crypto exposure, MSSE and MSOL are already priced to win the comparison.

Two timelines for the same bet

The bull case requires four or more weeks of combined ETH and SOL inflows alongside Bitcoin flows turning flat, with SOL weekly inflows moving from tens of millions toward hundreds of millions.

If that rotation arrives, 14 bps becomes a structural weapon: competitors running at 0.19% to 0.25% face the choice of cutting fees or ceding market share to a brand with Morgan Stanley’s distribution reach.

A fully staked SOL product retaining 95% of rewards at 14 bps makes the economics against a 20 bps unstaked competitor difficult to justify on the numbers alone.

The bear case is that the macro backdrop keeps institutions in Bitcoin-only or cash-equivalent exposures longer than the product filing timeline anticipates.

The Fed held the policy rate at 3.50% to 3.75% through mid-2026, with nearly half of policymakers projecting a possible rate hike for the year, and inflation forecasts revised higher.

In that environment, the allocation case for ETH and SOL as portfolio components faces a tighter cost-of-capital argument than it did in 2024.

Low fees and staking yields require an allocation case that advisors can justify to the client before inflows materialize.

The SEC’s effectiveness timeline adds a separate procedural layer of uncertainty: staking treatment, custody arrangements, and tax handling could all require further amendments before either product trades.

The prize Morgan Stanley is competing for is advisor shelf space in the allocation cycle that follows Bitcoin normalization.

By the time institutions broadly accept ETH and SOL as portfolio-eligible, Morgan Stanley crypto ETFs with low fees and staking pass-through could have a structural first-mover advantage.

The post Morgan Stanley’s proposed 0.14% ETH and SOL fees could turn the next crypto ETF race into a price fight appeared first on CryptoSlate.